Spotify Strategic Analysis: Business Growth Strategy

Analysis conducted for the Business Strategy Specialization: Business Growth Strategy course offered by UVA Darden School of Business on Coursera

Originally published on January 26, 2020.

Introduction

Spotify is an audio streaming service founded in 2005. Their stated mission is “to unlock the potential of human creativity by giving a million creative artists the opportunity to live off their art and billions of fans the opportunity to enjoy and be inspired by these creators”.

As written in the Spotify 2018 Annual Report (December 31, 2018), we find the service is available in 78 countries across the globe to 207,000,000 monthly active users (MAU). Within this user base, over 96,000,000 are Premium Subscribers which pay a monthly subscription for a set of features more advanced than the standard, free package.

In the previous three years ending December 31, Spotify demonstrated positive revenue growth as their free and paid user base expands:

· 2018: EUR 5,259,000,000

· 2017: EUR 4,090,000,000

· 2016: EUR 2,952,000,000

To populate it’s content library, Spotify has entered into license agreements with major and independent record labels or content creators: Universal Music, Warner Music Group, Sony Music Entertainment, and Merlin. Together these 4 organizations control the rights to sound recordings accounting for 85% of worldwide streams on Spotify.

Note: All supporting data for the introduction has been supplied from Spotify FY 2018 Annual Report (Citation 1)

Growth Analysis: Scenario Planning & Payoff Matrices

In recent years the music streaming industry has been marked by several trends:

· Since the advent of for-pay music streaming, the industry has been steadily adopted by music consumers as they realize the benefits of the streaming model compared to the traditional model of buying music CDs or MP3s

· Beyond simply replacing CDs and MP3 players, we see more and more evidence that Spotify is moving into consumers’ personal vehicles as connected cars begin to proliferate (Citation 2)

· Although Spotify’s primary reputation is as a music streaming platform, the amount of non-music audio content available to consumers continues to grow

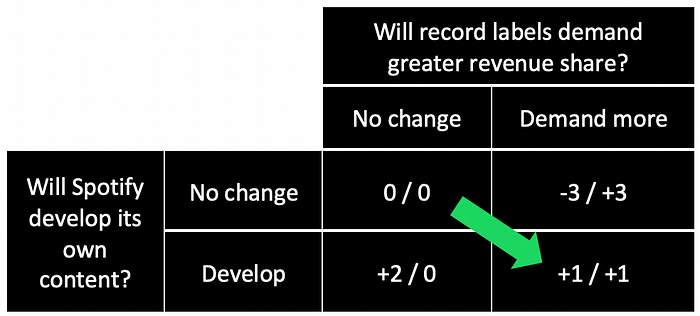

Still, Spotify and the industry face several future uncertainties (Citation 3):

· Will users convert from the freemium model to subscription users?

· Will record labels demand a greater share of music licensing revenues?

· Will Spotify develop its own in-house audio content creation capabilities?

Below we have selected two uncertainties to imagine potential growth scenarios for Spotify. We are choosing to use a timeframe of 2 years, which is equivalent to the length of time for the standard music licensing agreements.

Scenario 1 is the status quo. Spotify does not create its own content and the current licensing agreements state that music streaming revenues are split 30/70 with 30% of revenues going to Spotify and the remaining 70% going to record labels. These licensing agreements are negotiated every two years.

Scenario 2 represents a risk to Spotify’s current operations. In this situation, the record labels leverage Spotify’s reliance to increase their take of music streaming revenues. This would put a downward pressure on Spotify revenues, inhibiting their ability to continue international expansion and weakening their positioning to compete for users against competitors like Apple Music in global markets.

In scenario 3, Spotify begins to create content in-house. This represents a vertical integration of the industry value chain. Since Spotify already controls major distribution points such as Spotify editor playlists or being present on in-car infotainment systems, having access to their own content to distribute increases their power of bargaining against suppliers (the record labels).

Scenario 4 demonstrates movement by both companies into a heightened competitive environment where the record labels demand more revenue split for each stream and Spotify attempts to reduce its reliance on the record labels.

In order to understand their attractiveness, we have assigned payoffs to the different scenarios:

We current sit in the upper left quadrant (0 / 0), but when we consider expected future payoffs, we begin to realize that it is in the interest of both players to change the status quo in their favor. Thus, Spotify should move first to create more content in-house and establish greater independence from record labels who are likely to demand greater revenue share. We conclude that movement from the upper left quadrant into lower right quadrant where we see greater payoffs for both players (+1 / +1) is highly likely.

Growth Analysis: Acquisition Analysis

Unsurprisingly, in 2019 Spotify acquired two companies: Gimlet Media and Anchor Media (Citation 4). Gimlet media owns a number of popular podcast IPs and Anchor Media provides podcast creation, publishing, and monetization services (Citation 4)

We can utilize the acquisition analysis tool to better understand the composition of different variables and rationale behind Spotify’s thinking:

Strategic benefits:

• Actual independent value of both companies (revenue and profits are undisclosed)

• Added value: Ownership control of popular podcast IPs (industry roll-up), content production capabilities (vertical integration)

Cost of acquisition:

• Purchase price: $230,000,000 paid for Gimlet Media, $110,000,000 paid for Anchor Media

• Success costs: Integration costs, new overhead costs, learning curve of entering into new business operation

Opportunity Costs

• Building a stronger valuable competitive position through:

o Scaling of streaming business (user acquisition, increasing content library through licensing partnerships)

o Innovating new products and services to convert more users from freemium to paid model

o Growth through entry of new global markets.

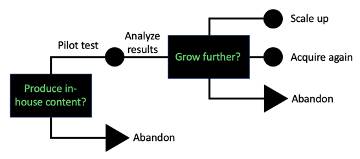

Growth Analysis: Real Options Analysis

The purchase of Gimlet and Anchor media are extremely strong signals of Spotify’s future path, and we expect Spotify to begin testing in-house content creation or marketing of new products to podcast creators at some point in the near future. Once the initial results are known, Spotify will have to make several decisions about whether to continue growing their content creation capabilities via scaling or acquisition or whether they should abandon this growth course and continue operating Spotify, Gimlet Media, and Anchor Media as independent companies.

As of the writing of this report, there have been no further updates on the use of Gimlet Media or Anchor Media since their acquisition.

Synthesis of Findings

Our analysis shows that we expect Spotify to continue down the path towards independence from music record labels and establish a greater presence as a content creator (or supplier). We may soon begin to hear about Spotify-created podcasts which will increase profit margins as there is no need to split revenues with external partners. However, this change would represent a new type of business for Spotify management, who has succeeded thus far as a technology and music distribution company. Given the expanding global user base, increased listening to non-music audio, and expected demand for greater revenue share from record labels, we are able to say with confidence that the move to acquire Gimlet Media and Anchor Media increases Spotify’s valuable competitive position. Still is unclear whether Spotify will be able to capture the potential economies from this acquisition for the deal to be considered a financial success in the long-run.

Sources Used:

2. https://www.gearbrain.com/spotify-in-car-how-to-2638712051.html

4. https://variety.com/2019/digital/news/spotify-podcast-gimlet-anchor-1203129844/

5. https://www.elon.edu/docs/e-web/academics/communications/research/vol8no1/10_Jason_Berk.pdf

6. https://marketrealist.com/2019/12/us-music-streaming-apple-music-and-spotify-dominate/